Report of the statutory auditor to the General Meeting of Liechtensteinische Landesbank Aktiengesellschaft Vaduz

Report on the audit of the consolidated financial statements

Opinion

As Group auditor, we have audited the consolidated financial statements (income statement, the statement of comprehensive income, balance sheet, statement of changes in equity, statement of cash flows and notes to the financial statements: pages 112 to 188) and the Group annual report (pages 110 to 111) of Liechtensteinische Landesbank Group (LLB Group) for the year ending as at 31 December 2016.

In our opinion, the accompanying consolidated financial statements give a true and fair view of the consolidated financial position in accordance with the International Financial Reporting Standards (IFRS) and comply with Liechtenstein law.

Basis for opinion

We conducted our audit in accordance with the standards promulgated by the profession in Liechtenstein and the International Standards on Auditing (ISAs), which require an audit to be planned and conducted so as to obtain reasonable assurance whether the consolidated financial statements and the Group annual report are free from material misstatement. We audited the items and disclosures in the consolidated financial statements by means of analyses and surveys on a sample basis.

Further, we assessed the application of the relevant accounting standards, significant decisions concerning the valuations and the presentation of the consolidated financial statements as a whole. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

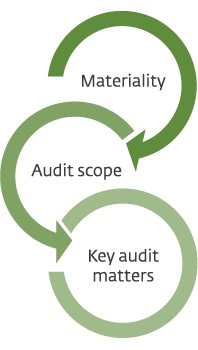

Our audit approach

Overview

Overall Group materiality: CHF 5.7 million

We concluded full scope audit work at four reporting units in two countries.

Our audit scope addressed 97 % of profit before tax and 99 % of the balance sheet total.

As key audit matters, the following areas of focus have been identified:

- Valuation of customer loans

- Impairment testing of goodwill

- Completeness and adequacy of the provisions for legal and litigation risks

Audit scope

We designed our audit by determining materiality and assessing the risks of material misstatement in the consolidated financial statements. In particular, we considered where subjective judgements were made. For example, in respect of significant accounting estimates that involved making assumptions and considering future events that are inherently uncertain. As in all of our audits, we also addressed the risk of management override of internal controls, including among other matters consideration of whether there was evidence of bias that represented a risk of material misstatement due to fraud.

We tailored the scope of our audit in order to perform sufficient work to enable us to provide an opinion on the consolidated financial statements as a whole, taking into account the structure of the Group, the accounting processes and controls, and the industry in which the Group operates.

Materiality

The scope of our audit was influenced by our application of materiality. Our audit opinion aims to provide reasonable assurance that the consolidated financial statements are free from material misstatement. Misstatements may arise due to fraud or error. They are considered material if, individually or in aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of the consolidated financial statements.

Based on our professional judgement, we determined certain quantitative thresholds for materiality, including the overall materiality for the consolidated financial statements as a whole as set out in the table below. These, together with qualitative considerations, helped us to determine the scope of our audit and the nature, timing and extent of our audit procedures and to evaluate the effect of misstatements, both individually and in aggregate on the consolidated financial statements as a whole.

|

Overall Group |

CHF 5.7 million |

|

|---|---|---|

|

materiality |

|

|

|

|

|

|

|

How we determined it |

5 % of profit before tax |

|

|

|

|

|

|

Rationale for the materiality benchmark applied |

We chose profit before tax as the benchmark because, in our view, it is the benchmark against which the performance of LLB Group is most commonly measured, and it is a generally accepted benchmark. |

We agreed with the Board of Directors that we would report to them misstatements above CHF 0.3 million identified during our audit as well as any misstatements below that amount which, in our view, warranted reporting for qualitative reasons.

Reporting on key audit matters

Key audit matters are those matters that, in our professional judgement, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Valuation of loans

Key audit matter

LLB Group grants loans to private individuals, corporates and public entities, primarily located in Liechtenstein and Switzerland.

Loans amount to CHF 11.5 billion (previous year: CHF 11.0 billion) and thus represent the largest asset item of LLB Group. Mortgage-based loans form the majority of the loan portfolio (86.5 % of total loans). In addition, LLB Group grants corporate loans and Lombard loans.

Any impairments are recognised by means of individual value adjustments. To this end, judgement has to be applied to calculate the amount of the individual value adjustment. We focused on the two following audit matters:

- The method used by LLB Group to identify any loans that may need adjusting, including loans that show indications of impairment according to the definition of LLB Group.

- The appropriate and consistent application of the policies and instructions issued by Group management relating to the calculation of the amount of the individual value adjustment.

The accounting and valuation principles applied to loans, the method used to identify the default risk and to determine the need for impairment as well as the evaluation of the coverage are taken from the management report.

Please refer to page 121 (accounting principles), page 134 (comments on the consolidated balance sheet) and page 174 (risk management in relation to credit risks).

How our audit addressed the key audit matter

We tested the adequacy and effectiveness of the following key controls relating to the valuation of customer loans:

- Credit processing and authorisation: Sample testing of the requirements and processes set out in the Group’s internal policies and working instructions in relation to credit processing. We also tested that authorisation is performed at the proper level in accordance with the system of authorities.

- Credit monitoring (periodic re-approval): Sample testing of identified bad debts and identifying the potential need for impairment.

Where significant judgement is required, we also put forward our own critical opinion as part of the substantive tests of detail on the authority to grant loans. Our tests of detail covered the following:

- Sample-based testing of new business and risk positions (including positions with individual value adjustments or indications of impairment) to evaluate whether additional value adjustments are needed.

- Sample-based testing of the method used to calculate value adjustments in terms of its appropriateness and compliance with the policies and working methods issued by the Group.

The combination of the audit of key controls and the tests of detail gives us sufficient assurance to assess the valuation of customer loans as adequate.

The assumptions used by LLB Group are in line with our expectations.

Impairment testing of goodwill

Key audit matter

The goodwill at the level of LLB Group in the Retail & Corporate Banking segment as at 31 December 2016 amounts to CHF 55.6 million (previous year: CHF 55.6 million) and originates from the acquisition of a subsidiary bank.

LLB Group performed impairment tests on the goodwill twice during the year. For the test, the value in use must be higher than the carrying amount. LLB Group uses a discounted cash flow (DCF) valuation method. The DCF method calculates the value in use based on the expected future cash flows. The method uses the following key assumptions and judgements:

- Assumptions regarding expected cash flows.

- Assumptions regarding the discount rate and the long-term growth rate.

Please refer to page 124 (accounting principles) and page 141 (comments on the consolidated balance sheet).

How our audit addressed the key audit matter

We based our audit on the analyses and calculations performed by Group management. With the involvement of a valuation expert, we performed the following audit procedures:

- Plausibility check of the analyses performed by LLB Group relating to the indications of a need for impairment.

- Assessment of the appropriateness of the DCF method and its implementation.

- Plausibility check of the medium-term planning of the subsidiary bank and an assessment of the expected cash flows by means of a target vs. actual comparison (backtesting).

- Plausibility check of the assumed growth rate and discount rate based on external market information.

- Tests of the sensitivity analysis of the applied parameters and assumptions.

The assumptions used by LLB Group are in line with our expectations.

Completeness and adequacy of the provisions for legal and litigation risks

Key audit matter

In the course of normal business, LLB Group is involved in various legal proceedings. The amount of the provisions for legal and litigation risks as of 31 December 2016 is CHF 47.0 million (previous year: CHF 24.0 million).

We identified the completeness and the adequacy of the provisions for legal and litigation risks as a key audit matter, as significant judgement exists in the assessment of the probability and the amount of the provisions for any financial obligations.

This includes processes to identify, evaluate and monitor client complaints as well as potential and actual legal proceedings. LLB Group creates provisions for actual and impending proceedings if, in the opinion of the specialists responsible, a cash outflow or a loss by the Group company is probable and the amount can be reliably estimated.

Please refer to page 125 (accounting principles), page 146 (comments on the consolidated balance sheet) and page 182 (risk management in relation to operational and legal risks).

How our audit addressed the key audit matter

We based our audit on the analyses performed by Group management. Further, we have referred to external lawyers’ letters. We compared the analyses with our own estimates and our understanding of the legal and litigation risks.

We performed the following audit procedures:

- Inquiries of the Head of Group Legal and specific Group management members.

- Review and inspection of the list of client complaints, correspondence with the regulatory authority as well as the minutes of the meetings of the Board of Directors and the Group management for indications of potential lawsuits.

- Review of the central inventory of current legal proceedings and sample testing of lawsuits with regard to the potential need for provisions.

- Obtaining external lawyers’ letters and expert opinions on selected ongoing lawsuits with regard to the probability and amount of the provisions, and comparing this with the provisions created by LLB Group as per the consolidated financial statements.

The assumptions used by LLB Group are in line with our expectations.

Other information in the annual report

The Board of Directors is responsible for the other information in the annual report. The other information comprises all information included in the annual report, but does not include the consolidated financial statements, the stand-alone financial statements and our auditor’s reports thereon.

Our opinion on the consolidated financial statements does not cover the other information in the annual report and we do not express any form of assurance conclusion thereon.

In connection with our audit of the consolidated financial statements, our responsibility is to read the other information in the annual report and, in doing so, consider whether the other information is materially inconsistent with the consolidated financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of the Board of Directors for the consolidated financial statements

The Board of Directors is responsible for the preparation of the consolidated financial statements that give a true and fair view in accordance with IFRS and the provisions of Liechtenstein law, and for such internal controls as the Board of Directors determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, the Board of Directors is responsible for assessing the Group’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the Board of Directors either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so.

Auditor’s responsibilities for the audit of the consolidated financial statements

Our objectives are to obtain reasonable assurance that the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Liechtenstein law and ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

As part of an audit in accordance with Liechtenstein law and ISAs, we exercise professional judgement and maintain professional scepticism throughout the audit. We also:

- Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal controls.

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made.

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group’s internal control.

- Conclude on the appropriateness of the Board of Directors’ use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group to cease to continue as a going concern.

- Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

- Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the Group audit. We remain solely responsible for our audit opinion.

We communicate with the Board of Directors or the Group Audit Committee regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide the Board of Directors or the Group Audit Committee with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence and, where applicable, related safeguards.

From the matters communicated with the Board of Directors or the Group Audit Committee, we determine those matters that were of most significance in the audit of the consolidated financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

Report on other legal and regulatory requirements

The consolidated management report is in accordance with the consolidated financial statements.

We recommend that the consolidated financial statements submitted to you be approved.

PricewaterhouseCoopers AG

Thomas Romer

Claudio Tettamanti

Auditor in charge

St. Gallen, 27 February 2017